How to Eat Your Competition for Breakfast

Counter-Positioning: rational choices and cognitive biases that paralyse businesses

The School of Knowledge is the weekly newsletter for SME owners and investors who want frameworks they can actually use — frameworks, checklists, and operating manuals every weekend, built to read on Sunday and use on Monday.

There are few occurrences in business as complex as the emergence and eventual success of a new business model. — Hamilton Helmer

After the First World War, the French built a line of concrete fortifications, obstacles, and weaponry along their border to protect themselves against the Germans, famously known as the Maginot Line. Up until the Second World War, war was almost predictable, slow, and recently fought in filthy trenches just metres from your enemy. You couldn’t blame André Maginot’s rationale for building the line — after all, it was the Germans who had been defeated the last time out.

But the Germans — bankrupt, embarrassed, and sent to the world’s metaphorical naughty corner — developed something so extraordinarily novel it birthed its own name: Blitzkrieg. And it was something else. The Maginot Line never stood a chance as the Germans ravaged their way through Europe to Paris, unfortunately developing its own signature branding: “For expensive things that offer a false sense of security.”

However, this isn’t a lesson on military ignorance: it’s about the most consequential Power in Hamilton Helmer’s 7 Powers. A Power whereby the incumbent can know of the novel business model, but declines to alter their strategy until it’s too late and they’ve been steamrolled. This Power is called Counter-Positioning.

This is the third deep-dive in the 7 Powers series — Hamilton Helmer’s landmark book on how businesses use strategy and value to create consistent differential returns—something he calls Power. In the introductory article, I explained why value creation alone isn’t a moat; in the first deep-dive, I covered Scale Economies; in the second, we examined Network Economies. Let’s now get into the third Power: Counter-Positioning.

What is Counter-Positioning?

A newcomer adopts a new, superior business model which the incumbent does not mimic due to anticipated damage to their existing business. — Hamilton Helmer

Jack C. Bogle had a radical new idea: an equity fund that simply tracked the market. On May 1st, 1975, he managed to persuade a reluctant Wellington Management board to back his company, Vanguard. Up until then, funds had been run by managers who collected fees and commissions — but Bogle’s Vanguard would operate at cost, return all profits to fundholders, and eventually abolish sale commissions.

The idea didn’t go down well — initial subscriptions reached just $11 million by 1976. The sticking point was that Bogle needed brokers to help distribute the fund, but the fund’s premise was centred around not needing their input. It’s hard to get people to do things for you when they have no self-interest.

And just like the French were thinking rationally when they built the Maginot Line, it’s easy to see why the active management firm Fidelity weren’t interested in this new business model. No star fund managers, no research department, and an unwillingness to attempt to beat the market — it went against everything that made Fidelity what it was.

Fidelity were awake to the threat alright — they just fancied their model more than Vanguard’s. That’s what Counter-Positioning actually is: the incumbent knowingly decides against adopting the new business model. And it’s far more unsettling for investors than a story about incumbent blindness.

The Mechanisms of Counter-Positioning

Compared to Vanguard, Fidelity Investments possessed a structural disadvantage: they had to consistently beat the market before deducting their fees to arrive at the same place Vanguard was aiming for — to track the index. That’s no small task, and Fidelity was fighting against three forms of collateral damage:

Revenue cannibalisation: Vanguard directly ate into Fidelity’s active management fees by offering customers a way to circumvent them entirely — opting for Vanguard’s fund instead. This is similar to how Blockbuster relied on late fees (50% of revenue) and Netflix came along with a superior model: digital rental and no late fees.

Distribution destruction: The new model undermined Fidelity’s reliance on brokers, who collected their fees regardless of how well the fund performed.

Identity destruction: The most powerful of the three. Fidelity’s whole mythology was built on the premise that people needed their expertise — their star managers, their research, their brokers. Admitting that Vanguard had a superior model wasn’t just breaking a historical promise to customers: it was questioning the very identity of the company. Some businesses just can’t look themselves in the mirror.

Benefits and Barriers

The benefit

The new business model is superior to the existing one by offering considerably lower costs, or the ability to charge higher prices. For Vanguard, they completely negated portfolio manager fees, broker fees, and trading costs simply by not needing their ‘expertise’. Along with returning profits to fund-holders, this allowed Vanguard to take market share from Fidelity.

The barrier

Compared to the other Powers, the barrier for Counter-Positioning is a tad more mysterious. The barrier is formed from the incumbent’s own willingness to deliberately not engage with the newer business model, believing the potential returns are inferior to their legacy model and won’t make up the collateral damage from switching. Their existing model acts as a prison. It wasn’t that Fidelity were caught on their toes, or lacked foresight — it was determined through a thoughtful, calculated process that ultimately concluded they just couldn’t switch financially. A rational decision by any means.

“Why would anyone settle for average returns?” — Ned Johnson, Fidelity

Case Study: Vanguard

So how did Bogle’s bold move in 1976 pan out? Let’s look at Vanguard’s assets under management (AUM):

August 1976: $11M at launch

Mid-1977: $17M (Helmer’s figure, from the book)

End of 2015: $3T (Helmer’s figure, from the book)

December 2025: $12 trillion total, of which $10.1 trillion is index assets and $1.9 trillion is active1

That progression — from $11 million to $12 trillion over nearly 50 years — is one of the most dramatic compounding stories in financial history. If we calculate the CAGR:

CAGR = (12,000,000 / 11)^(1/49) − 1 = approximately 32.8% per year

(Both figures expressed in $M: $12 trillion = $12,000,000M; starting AUM = $11M)

But it’s important to note a caveat: this isn’t an investment return. It’s a measure of business growth — AUM expansion driven by two compounding forces simultaneously: market appreciation on existing assets, and net new inflows as investors moved from active to passive. What the CAGR captures is the combined effect of a superior product attracting capital while the incumbent was rationally paralysed. Every year Fidelity decided not to fully replicate Vanguard’s model, more assets migrated. The CAGR isn’t measuring Vanguard’s investment skill — it’s measuring the rate at which the Counter-Position compounded against Fidelity.

Fidelity’s rational decision not to engage with the new model may have been smart in the short term, but catastrophic long term.

The fee cliff

It wasn’t until 2018 that Fidelity launched their Zero funds2, introducing a 0% expense ratio to compete with low-cost index providers. Just 42 years later.

Interestingly, average expense ratios increased through the 80s and 90s, rising to an average of 1.04% in 1996. The incumbent active funds weren’t even cutting fees in response — they were raising them. Eventually, passive investing became impossible to ignore, and by 2021 expense ratios had fallen to approximately 0.46% compared to 0.06% for index funds — a gap of roughly 7.5x.

Fidelity manages roughly $5.4 trillion in discretionary AUM today. At a blended active fee of even 0.50%, that’s $27 billion in annual fee revenue. Vanguard’s average expense ratio across its $12 trillion AUM is approximately 0.05–0.06%, producing around $6 billion in revenue despite managing more than twice the assets. That gap — $27B vs $6B on comparable AUM — is the collateral damage number made concrete. You could argue that Fidelity would have been foolish to move into passive indexing any sooner than they did.

That’s what makes Counter-Positioning as a Power so interesting. The incumbent can survive — thrive even — but they are rationally unwilling to copy the new entrant because the numbers don’t math the way they want them to math. Fidelity survived. Blockbuster did not.

The distribution network problem

Not only did the numbers not stack up, but Fidelity was built on incentives. Active fund managers were paid well for beating the market, advisors earned a commission for getting customers to move money into Fidelity’s funds, and brokers collected fees for sorting out the admin. It was a win-win-win for all involved. And besides, most people who invest in funds look at total fees of, say, 2–3% per year and think: that’s not a bad deal, is it? It’s only when you do the maths and see the compound effect of those fees over 30 years that you start to have a heart attack.

Better to do that maths in your healthier years, i’d say.

For Fidelity to have entered this market in the mid-seventies would have meant a complete reconstruction of their foundations, and from being in the construction industry i can tell you one thing: if you need to change your foundations, whatever’s sitting on top of them — a building, a business model — has to come down.

The identity trap

Most interesting, i think, is how it would have looked if Fidelity had changed course. A prestigious firm with ‘world-class’ portfolio managers suddenly tells customers: “we actually think we’ve found something better — and guess what, it’s practically free.” Maybe great for those just signing up, but a potential headache for those already heavily invested. Having a reputation to uphold is costly.

So, Fidelity saw exactly what Vanguard was doing. They had the capital, the distribution, the brand, and the talent to respond. They understood the new model completely. So why did it take them over forty years to copy them?

In the paid section, i look to answer this question, along with:

The precise calculation Fidelity made — and why it was rational, not lazy

Helmer’s decision tree for evaluating any Counter-Position — and what it reveals about durability

The three ways incumbents fail to respond: Milk, History’s Slave, and Job Security — and why only one of them is investable

How to calculate whether a Counter-Position will hold or collapse

Six red flags to watch out for that tell you if Counter-Positioning will fail

Where weak versions of this Power appear — and what they’re actually worth

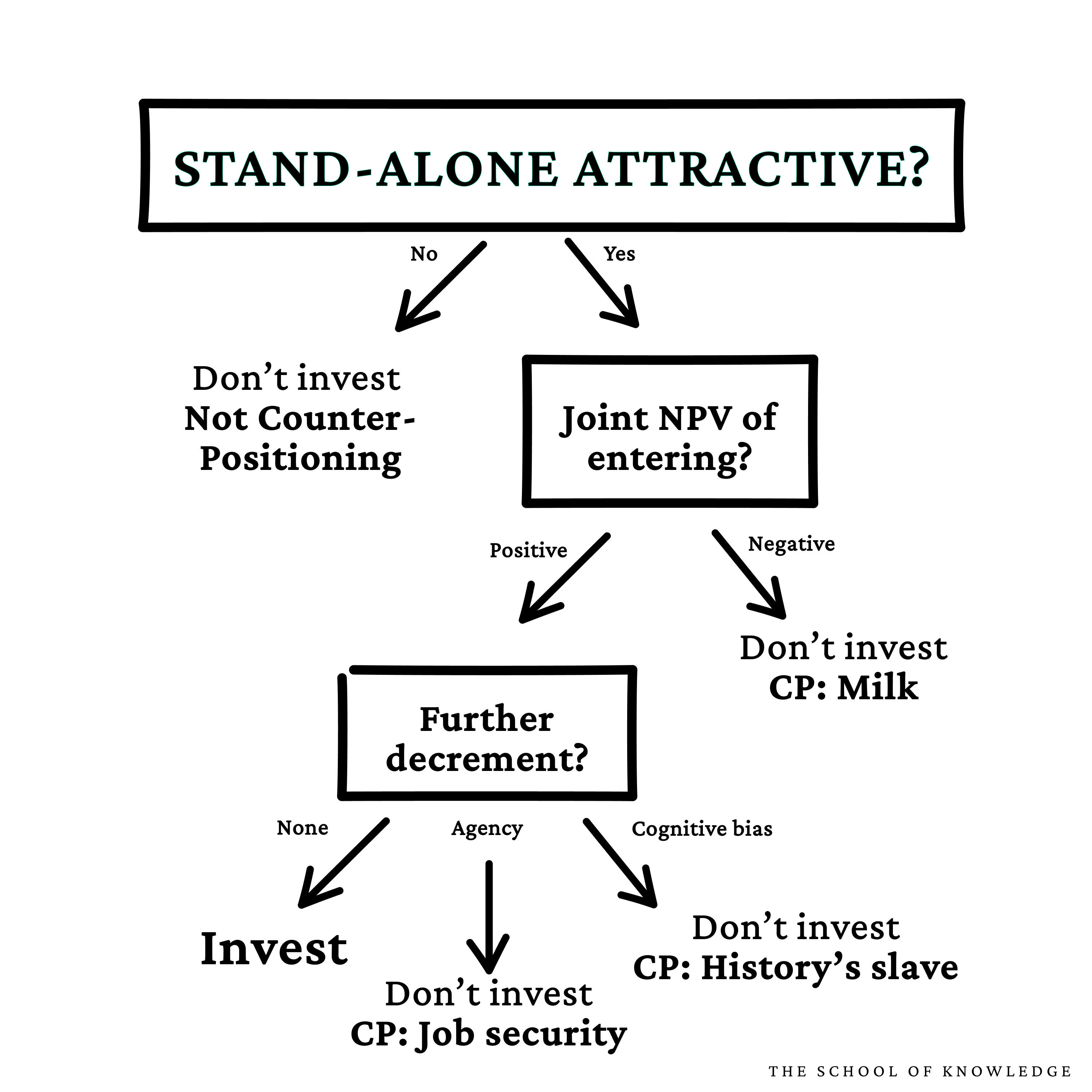

Helmer’s Decision Tree: The Taxonomy of Incumbent Failure

Stand-alone attractive?